Tech and SaaS multiples in Q4

Below are revenue multiples for publicly traded consumer tech companies (B2C). Industries and therefore multiples vary widely. Commentary is below. If you’re looking for data on SaaS multiples, keep scrolling.

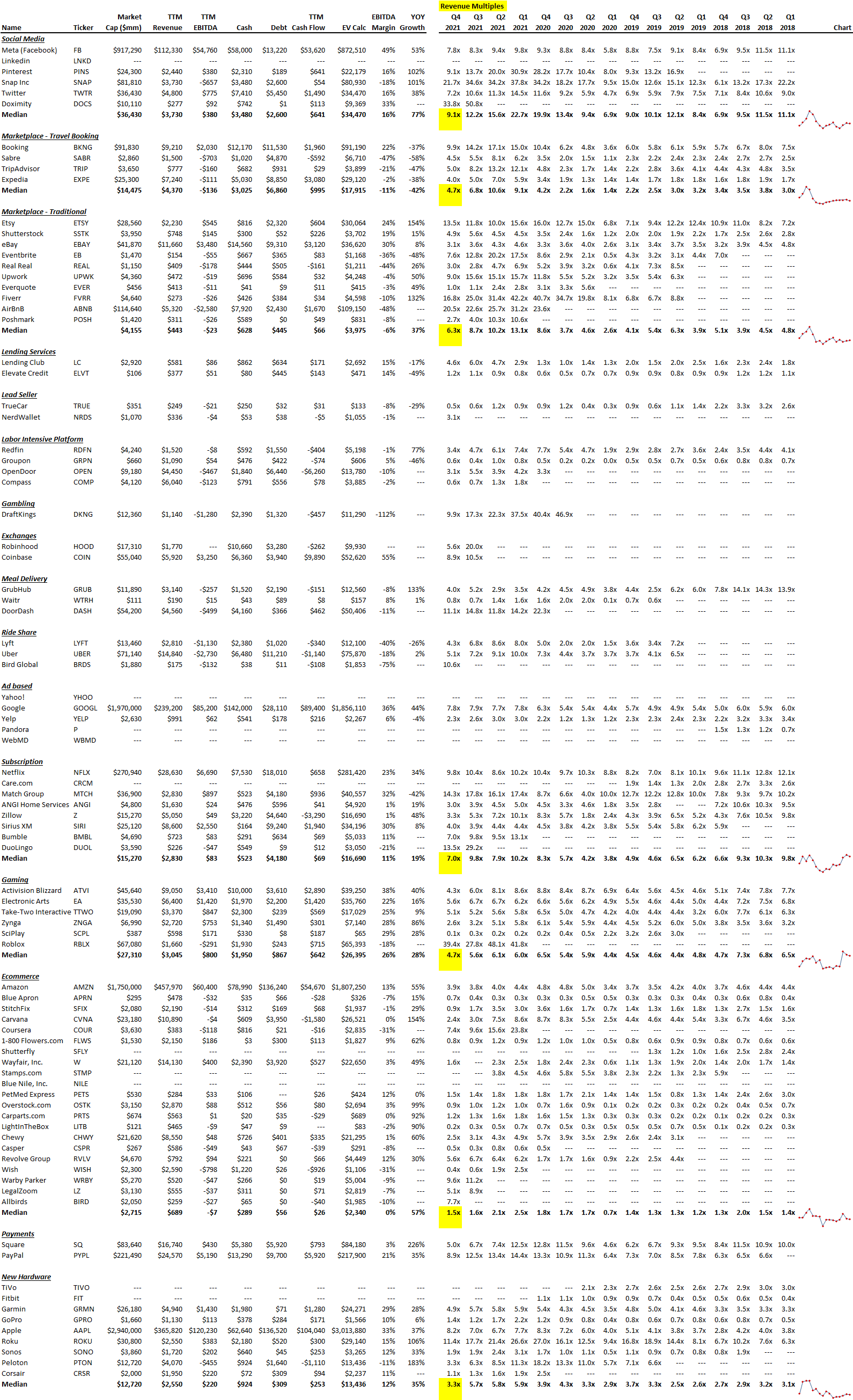

Social media is back to 2020 levels. Multiples rose steadily through 2020 peaking at 22.7x on median in Q1 2021. Q4 is showing 9.1x. YOY growth in the space is fantastic (77% on median), with Snap and Pinterest leading the way (80%+ YOY growth). Facebook is still the monster in the space with $112bln of annual revenue and a phenomenal EBITDA margin (49%). The newcomer, Doximity, is trading at 34x, which doesn’t seem sustainable relative to peers.

Travel marketplaces are still strong at 4.7x. Multiples hit 10.6x in Q2 2021 which is remarkable for a business that traditionally trades no greater than ~3x. Booking.com is trading at an especially strong 9.9x and is the only company to maintain its profitability over the last 12 months ($997mm).

Traditional marketplace multiples vary widely. Prior to Q3 2018, the sector only had 2 companies and now has 10. The median multiple is now 6.3x, but Etsy, Fiverr and AirBnB have extraordinary multiples (14x. 17x and 21x). Etsy grows 154% YOY with $2.2bln of revenue, and a solid 24% EBITDA margin. The multiples for these top performers are very high, whereas flatter growth cash generators like Shutterttock and eBay trade at 3x to 5x. AirBnB is unprofitable with an anemic EBITDA margin of -48%, but positive cash flow thanks to deposits.

Labor intensive space. The only reason we even include these companies in our analysis is because investors like Softbank insist on labelling these services businesses as tech co’s. At best, they’re tech enabled which isn’t the same thing at all. Remember when Groupon was a high flier? Well today it’s shrinking (-46% YOY growth) and trades at 0.6x revenue. Cash on the books represents more than half the market cap. This was one of the fastest growing companies ever that came up during the recession of ’08, and now no one cares. Redfin and Opendoor feel especially overvalued. OpenDoor, Redfin, and Compass don’t make money, which is a very dangerous place to be for services businesses of their size.

Other Outliers. DraftKings trades at 10x its $1.1bln of revenue and has a horrendous -112% EBITDA margin. DoorDash trades at 11x it’s $4.5bln in revenue.

Rideshare multiples coming in. Lyft is at 4.3x revenue while Uber is at 5.1x revenue. We suspect the revenue multiple for both would be higher, but both businesses light cash on fire. Lyft’s EBITDA margin is -40% and Uber’s is -18%. It’s hard to envision either company generating cash any time in the near future given their current market share and very high levels of burn, and keep in mind food delivery saved Uber during 2020. Bird is trading at 11x even though their business model is broken.

Subscription. B2C subscription is an excellent business model and trades at 7x revenue, which frankly is pretty reasonable relative to the rest of the group. Match is at 14x revenue, Bumbl is at 7x. Bumbl and Match both have wonderful profitability and high margins (11% and 32% respectively). Duolingo which is new to the group trades at 14x.

Gaming. The median revenue multiple of 4.7x is strong. SciPlay is an underperformer at 0.1x while Roblox is at a very high 39x while being the only cash burner in the group. In 2021 Roblox just got hit with a $200mm lawsuit over music rights (June 2021).

Ecommerce is varied. The sector is the least attractive to investors, with a median revenue multiple of 1.5x. There is a big difference between what we would call premium ecommerce like Carvana, Allbirds, Coursera, Chewy, Warby, LegalZoom, and Amazon, versus weak ecommerce like Blue Apron (0.7x revenue). Chewy has excellent customer retention metrics and will likely be a premium ecom player for years to come, if not a nice acquisition target. Note that the margins in ecommerce are really tight with a median EBITDA margin of 0%. Amazon is at 13%, but $14bln of their $23bln of 2020 operating income (61%) came from AWS, whereas AWS was $45bln of their $386bln of net sales in 2020 (12%).

Hardware is elevated at 3.3x. Roku is the standout of the group (11x) as it’s growing at a strong 106% YOY. Peloton trades at 3.3x on 183% YOY growth thanks to covid. Apple’s growth is 37%, very strong for a company with $365bln in annual sales and a 33% margin. They recently had a $3trln market cap.

SaaS

SaaS comps continue to be strong, but fell from last quarter. Of the 126 SaaS companies we follow, the average public SaaS business is trading at 17.9x revenue while the median is 12.2x. In Q3, the average was 20.0x.

The gap between the average and median is 5.7x, meaning premium SaaS companies are getting outlier valuations. 54% of companies are trading at 10x revenue or greater. The data is below.

Negative EBITDA, positive cash flow. The median SaaS business had trailing twelve month revenue of $427mm, EBITDA of -$16mm, but positive operating cash flow of $42mm thanks to up-front collections on annual contracts. So long as you’re growing (the median annual growth rate is 23%), investors will overlook negative EBITDA especially if the business is cash flow positive after working capital changes.

The trend is still on. The chart in the picture shows median revenue multiples we’ve collected since Q4 2014. During that period, the median SaaS multiple has ranged from 4.6x to 14.1x with an average of 8.4x.

SaaS margins are still terrible. Investors and founders love saying “SaaS margins are great.” They’re not. They’re horrible. The median EBITDA margin for the companies above was -3%. Fixed costs for SaaS are terribly high and worse yet, those fixed costs are mostly people, meaning the only way to materially cut costs is layoffs. If you’ve ever fired someone, you know cutting costs by cutting people is not easy and hurts the culture and morale of remaining members.

Premium gets a premium. Premium SaaS businesses trade at premium multiples. In the data set, 68 companies trade at greater than 10x revenue, 50 trade at greater than 15x, and 37 trade at greater than 20x.

Growth is strong. The median of 23% is good given the size of these companies. The average is even better at 27%.

SaaS businesses are healthy. There is almost no debt on these businesses (except McAfee) as banks don’t like ‘asset-lite’ businesses like software. Additionally, these companies have $402mm of cash on the balance sheet on median, plenty relative to annual burn (recall EBITDA is -$16mm). The number of years of cash on the balance sheet is less important given that these businesses are generally cash flow positive (median of $42mm); only 35 out of the 126 companies have negative cash flow. Note that 69 out of the 126 have negative EBITDA, but again that’s acceptable so long as the growth is present and cash flow overall is positive.

Recent IPO’s are killing it. Some of the latest IPO’s are trading at unreal multiples: Hashicorp is at 52x, Braze is at 29x, Gitlab is at 49x, and Amplitude is at 41x. Some recent IPO’s are trading at more reasonable multiples, so the disparity in valuation for premium SaaS versus just good SaaS is very wide.

Visit us at blossomstreetventures.com and email me directly at sammy@blossomstreetventures.com. All founders and funds welcome! We invest in companies with run rate revenue of $2mm to $30mm, with year over year growth of 20% to 50%+ depending on revenue. We lead or follow in growth rounds and special situations like inside rounds, small rounds, rushed rounds, corralling investors with our term sheet, bridges, inbetweeners, cap table clean up, and extensions. We can commit in 3 weeks and our check is $1mm to $3mm. Also visit https://blossomstreetventures.com/metrics/ for always updated SaaS metrics.