SaaS multiples now below 5x

SaaS valuations haven’t been this low since Q4 2015. Of the 119 SaaS companies we follow, the median public SaaS business is trading at 4.9x revenue while the average is 5.95x. The gap between the average and median is only 1.0x, meaning premium SaaS companies are getting slightly higher valuations, but that gap is the lowest since Q2 2018, showing the correction in overvalued names.

Multiples for SaaS companies growing above the median of 24% are better: 6.5x on median and 7.6x on average. Only 16% of companies are trading at 10x revenue or greater, whereas the peak was 60% in Q4 2020. Only 1 company trades above 20xm whereas 35 traded above 20x in Q4 2020. The data is below.

Additional observations are as follows:

Negative EBITDA, positive cash flow. The median SaaS business had trailing twelve month revenue of $537mm, EBITDA of -$58mm, but positive operating cash flow of $28mm thanks to up-front collections on annual contracts. So long as you’re growing cash efficiently (the median annual growth rate is 24%), investors will overlook negative EBITDA especially if the business is cash flow positive after working capital changes.

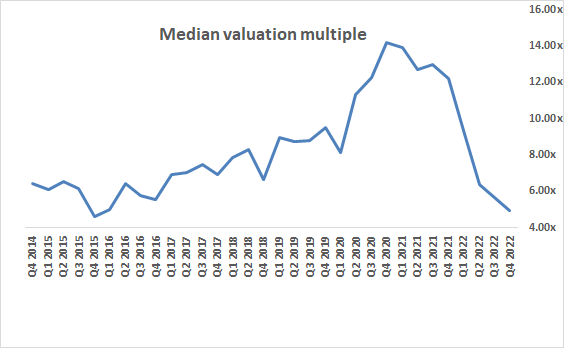

The trend. The chart below shows median revenue multiples we’ve collected since Q4 2014. During that period, the median SaaS multiple has ranged from 4.6x to 14.1x with an average of 8.2x.

SaaS margins are still terrible. Investors and founders love saying “SaaS margins are great.” They’re not. They’re horrible. The median EBITDA margin for the companies above was -13%. Fixed costs for SaaS are high and those fixed costs are mostly people, meaning the only way to materially cut costs is layoffs.

Premium gets a premium. Premium SaaS businesses trade at premium multiples, but the number of premiums is shrinking. In the data set, 19 companies trade at greater than 10x+ revenue, only 2 trade at greater than 15x, and only 1 trades at greater than 20x.

Growth is strong. The median of 24% is good given the size of these companies. The average is 25%.

SaaS businesses are healthy. There is less debt on the books ($275mm median) than cash ($459mm median). Median cash of $459mm is 8 years of burn at the current level of EBITDA (-$58mm median). The number of years of cash on the balance sheet is less important given that these businesses are generally cash flow positive (median of $28mm); only 41 out of the 119 companies have negative cash flow. Note that 76 out of the 119 have negative EBITDA, but again that’s acceptable so long as the growth is present and cash flow overall is positive.

Visit us at blossomstreetventures.com and email me directly at sammy@blossomstreetventures.com. All founders and funds welcome! We invest in companies with run rate revenue of $3mm to $30mm, with year over year growth of 20% to 50%+ depending on revenue. We lead or follow in growth rounds and special situations like inside rounds, small rounds, rushed rounds, corralling investors with our term sheet, bridges, inbetweeners, cap table clean up, and extensions. We can commit in 3 weeks and our check is $1mm to $4mm. Also visit https://blossomstreetventures.com/metrics/ for always up-to-date SaaS metrics.