Q4 SaaS Multiples up!

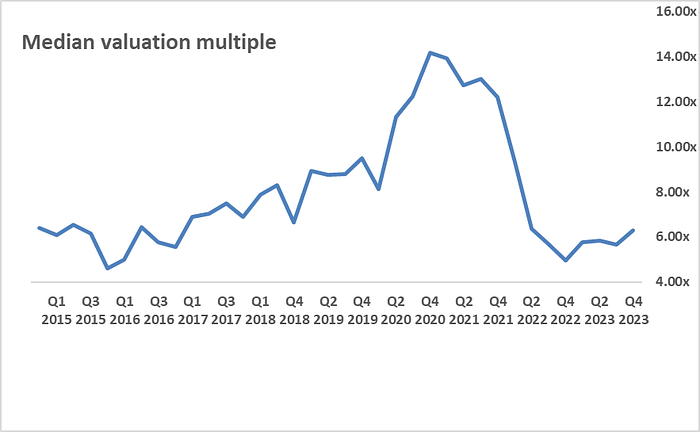

SaaS multiples had a great Q4 relative to Q3. Of the 110 publicly traded SaaS companies we follow, the median multiple is 6.30x revenue while the average is 753x. Multiples for SaaS companies growing above the median of 18% are far stronger: 8.98x on median and 10.11x on average. Overall the multiples made a big move from Q3, and these are very healthy levels for SaaS companies generally. The data is below.

Additional observations are as follows:

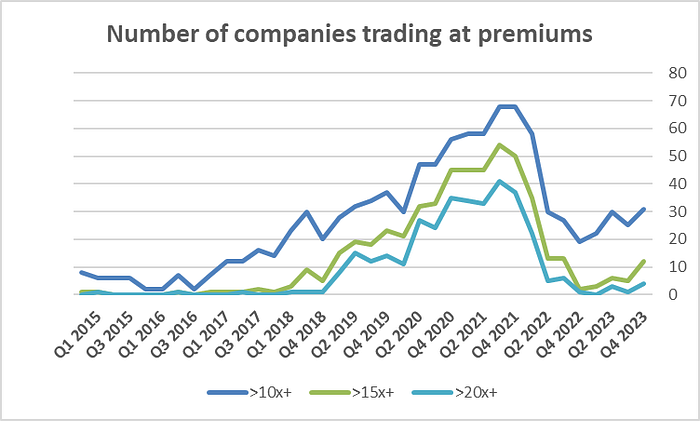

The heyday of 2020 has not returned. 28% of companies are trading at 10x revenue or greater, whereas the peak was 60% in Q4 2020. Four companies trade above 20x whereas 35 traded above 20x in Q4 2020. Additionally, the gap between the average and median is only 1.2x, meaning premium SaaS companies are getting slightly higher valuations, but that gap is tight relative to 2020 and 2021 when it was ~5.8x.

The stats. The median SaaS business had trailing twelve month revenue of $668mm, EBITDA of -$24mm, but positive operating cash flow of $93mm thanks to up-front collections on annual contracts. YOY growth is 18% on median. The median EBITDA margin is -4%. Debt is negligible. While 62 of the companies have negative EBITDA, only 27 have negative cash flow.

The trend. The chart below shows median revenue multiples we’ve collected since Q4 2014. During that period, the median SaaS multiple has ranged from 4.6x to 14.1x with an average of 7.9x.

Premium gets a premium. Premium SaaS businesses trade at premium multiples, but the number of premiums is shrinking. In the data set, 31 companies trade at greater than 10x+ revenue, 12 trade greater than 15x, and 4 trade greater than 20x.

Thank you for your readership. Visit us at blossomstreetventures.com for more data and blogs.